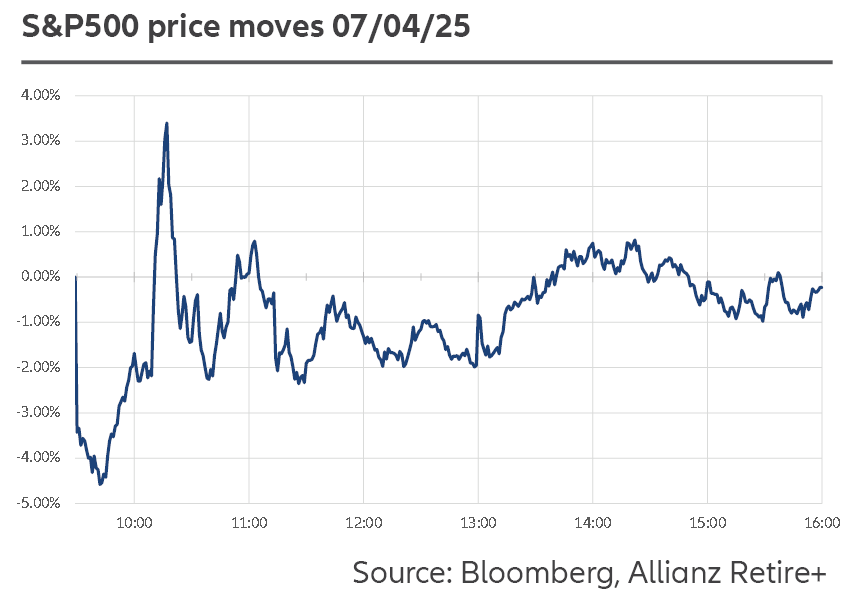

What’s going on?

Optimistically, this could be a strategic negotiation by Trump, akin to his approach with Ukraine and Russia. He has expressed openness to tariff negotiations, a sentiment echoed by his administration. If this holds true, Trump aims to rebalance the US trade deficit by engaging countries individually. Nations like Vietnam, Cambodia, India, Australia and Mexico have cooperated while others, such as China and the EU, have not. Expect minor pyrrhic victories over diminutive trading partners to be celebrated this week by Trump.

A secondary ambition of the Trump administration may be to engineer a ‘recessionary shock’—not a full recession—to force the Federal Reserve’s hand to lower domestic borrowing costs and even invoke quantitative easing measures. This delicate balance between growth and inflationary expectations versus international confidence is a bold move.

Why is Trump playing Russian roulette?

Trump’s tariffs aim to raise $6 trillion from other countries and spark a manufacturing boom with high-paying jobs. Yet, these outcomes are largely mutually exclusive. If the USA collects this amount, it’s because foreign goods continue to be purchased, negating a manufacturing revival. Conversely, reviving manufacturing and halting imports would prevent the USA from collecting additional revenue. The notion that the USA doesn’t manufacture is false. US manufacturing is at record highs, but automation has claimed jobs, not Mexico or Canada. More manufacturing won’t equate to more jobs; it will mean more robots working overtime. Tariffs make building factories in the USA expensive, with components tariffed and hiring challenging due to near-full employment and immigration cuts.

The broader implications

Modern economies are consumer-led, interconnected, and sentiment-driven, especially in post-COVID hyper-liquid markets. The uncertainty will directly and immediately cost businesses as they navigate alternative trading partners. Major trading partners like China and Japan have been preparing for months.

An overlooked element in this discussion, is that the USA’s trade deficit also brings a current account deficit. America’s ‘exorbitant privilege’ of printing the world’s reserve currency allows borrowing to finance consumption at favourable rates. Foreigners pay in dollars, not Euros or Yuan, granting the USA effectively an interest-free loan. The longer these trade wars continue, the higher the risk to the US foreign reserve currency status.

Looking ahead

Trump may reverse tariffs individually at any moment.

The assumption that tariffs will drive local industry adaptation requires permanence, a concept rarely associated with Trump. Heavy capital investments generally demand certainty beyond political cycles.

While the Chinese are escalating tariffs, we expect the response of European governments and corporations will pose the largest existential threat to the continuation of current US protectionist policy. Those interested in the human and financial outcomes of economic policy have much to consider with this potential dramatic re-alignment of the world trade order. Market participants may well run out of hyperboles by the end of the week.

Martin Wilkinson

Head of Investments

martin.e.wilkinson@allianz.com.au

Adam Downy

Investment Analyst

adam.j.downy@allianz.com.au

Allianz Retire+ is a registered business name of Allianz Australia Life Insurance Limited ABN 27 076 033 782, AFSL 296559. This information contains opinions that are current as at April 2025 unless otherwise specified and is for general information purposes only and is not comprehensive or intended to give financial product advice. Any advice provided in this material does not take into account your objectives, financial situation or needs. No person should rely on the content of this material or act on the basis of anything stated in this material. Allianz Retire+ and its related entities, agents or employees do not accept any liability for any loss arising whether directly or indirectly from any use of this material.