Interest rates up and equities to the moon . . . how much longer before gravity kicks in?

Key Points

- Bond and equity markets are sending conflicting signals

- The era of cheap capital is over; structural forces are keeping interest rates higher for longer

- Pre-conditions for a bubble in US equities are present

- Higher rates historically trigger severe equity drawdowns and prolonged recoveries

For much of this century, cheap capital allowed businesses to borrow easily and prioritise growth over profitability. 5000-year lows in interest rates, extraordinary actions by central banks and abundant liquidity meant that growth was almost indiscriminately funded, leading to the advent of such things as tech unicorns, zombie companies and promises of datacentres on Mars!

Today’s market looks different. Capital is more expensive as central banks push borrowing costs higher. The latest global hiking cycle has commenced with liquidity slowing globally, compounding the impact. Excess household and corporate savings amassed post-COVID era have largely been eroded.

Concurrently, a transformative technology is ascending. AI has already required the biggest infrastructure spend in the history of financial markets. Notably, the underlying technology is increasingly funded by debt (and less by earnings and equity) meaning not only do these investments require higher earnings to reward investors, but systemic risk is rising from broader debt exposures.

However, AI is not the only growth sector competing for capital in 2026. We are also seeing a ramp up in defence spending, a capital-intensive energy transition and a geopolitical environment where global supply chains are relatively more focused on security over efficiency. This dynamic is further exacerbated by larger government spending manifesting in rising deficits, the outcome of which is simply that to achieve equilibrium, higher real rates are required.

Notions that guided past decades look increasingly antiquated – namely that the world has a savings glut and suffers from lack of demand. Central banks have run out of adjectives in the 2020s when trying to relegate inflation as a temporary phenomenon (‘transitory’, ‘transient’) while investors are left to consider – under this new macro-economic regime, what threat does a prolonged higher rate environment pose to portfolios?

So what? The challenge for investors

Equity bubbles are not directly caused by technological developments or funding alone, but rather historically form around speculative froth and market excesses. Whether the supercharged performance in US equities is a bubble or not, it’s impossible to tell. More important for investors to note is that the two pre-conditions of a bubble – namely speculative behaviour and extreme valuations – are present. The recent SpaceX IPO is a telling example. After launching at a hefty price-to-sales ratio of 90, it has since soared to a ratio of over 120. For comparison, Google’s public offering in 2004 traded at roughly 10-times present year sales. Apparently, if a company is involved in a sexy sector (i.e. AI or space tech), investors seem to have little regard for valuations.

Large cap US equities surged in the last quarter to end the Australian financial year with the S&P 500 returning ~15% and the NASDAQ returning ~21% for the quarter, primarily fuelled by a massive rally in semiconductor and AI-related stocks. This was the best quarterly performance in six years for both indexes, building on strong double-digit returns in the two years prior. US equities growth has been hot for several years, and gains increasingly concentrated. The 10 biggest companies now account for 38% of the S&P 500, up from 25.6% in June 2020.

It is prudent for investors to remind themselves that, while equities trend higher over the longer term, they are inherently cyclical, repeatedly rising above and falling below their long-term trend. Cyclical fluctuations are a key aspect of investment markets. Most are driven by economic developments but get magnified by swings in investor sentiment.

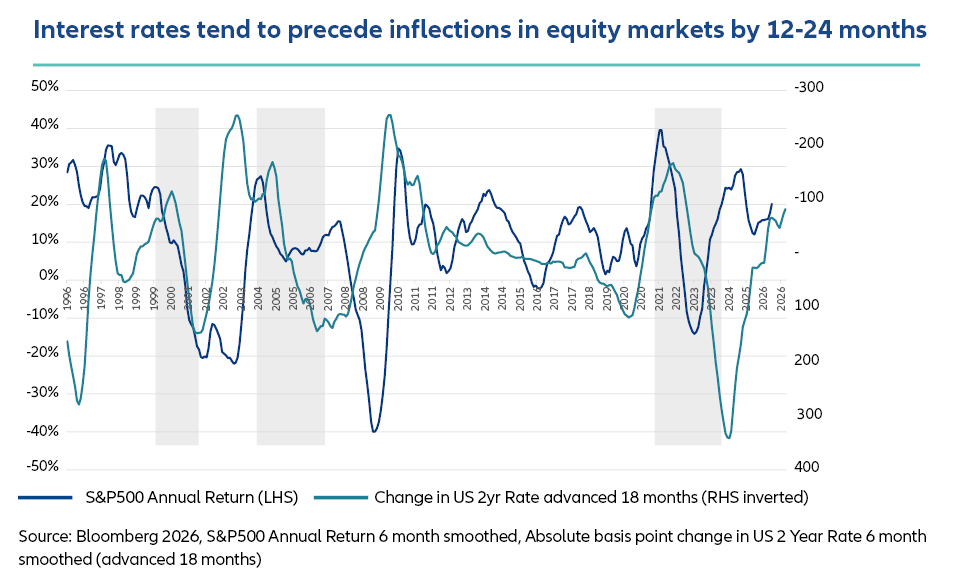

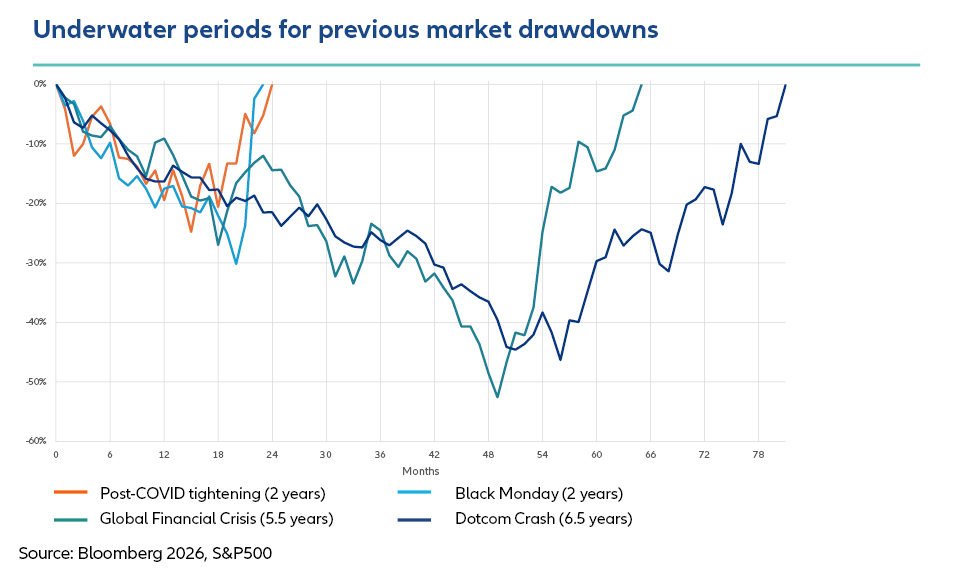

The global environment of ongoing higher interest rates should mean higher discount rates for equity growth. Higher rates have also historically been a frequent catalyst for causing severe drawdowns or bear markets in equities, which can reverse years’ worth of gains, resetting short-term exuberance back to more fundamentally orientated levels. While bear markets tend to be short-lived (with the average length of 289 days or 9.6 months), some are much longer (see chart below).

Conclusion

Prior to the 2020s, most investors did not need to consider the impact of a moderate inflationary environment and prolonged higher interest rates. 2026 presents a remarkably different environment. Structural drivers are leading towards a prolonged paradigm shift, for which many portfolios are untested and underprepared.

In such an environment, downside protection becomes paramount. Fixed income becomes more regime dependent, and the relative certainty of portfolio income should be assessed by investors considering a potential equity market crash or increase in credit defaults. Historically, equities have taken several years to recover previous highs in the event of meaningful drawdowns in equity markets.

Being aware of elevated sequencing risk does not mean one has to position for apocalypse. Positioning for market fragility and the possibility of a correction is prudent. Rather than simply diversifying, investors should consider options to genuinely mitigate sequencing risk — protecting accumulated gains while maintaining exposure to future growth.

Allianz Retire+ is a registered business name of Allianz Australia Life Insurance Limited ABN 27 076 033 782, AFSL 296559. This information contains opinions that are current as at July 2026 unless otherwise specified and is for general information purposes only and is not comprehensive or intended to give financial product advice. Any advice provided in this material does not take into account your objectives, financial situation or needs. No person should rely on the content of this material or act on the basis of anything stated in this material. Allianz Retire+ and its related entities, agents or employees do not accept any liability for any loss arising whether directly or indirectly from any use of this material. Past performance is not a reliable indicator of future performance.

We’re here to help.

Call or email us for assistance.

Any information on this website does not take into account your objectives, financial situation or needs. For personal financial advice please speak to your financial adviser. Products will be issued by Allianz Australia Life Insurance Limited, ABN 27 076 033 782, AFSL 296559.

Allianz Retire+ is the business name of Allianz Australia Life Insurance Limited. By using this website you agree to access this Financial Services Guide.

Allianz Retire+ is the business name of Allianz Australia Life Insurance Limited. By using this website you agree to access this Financial Services Guide.